Private lending can be an effective alternative to traditional finance, but informal or unclear arrangements often lead to costly disputes – something we can help you avoid.

If you are lending money privately, or are owed a debt, our dispute resolution legal experts can help you protect your position and improve your prospects of recovery.

Our team specialises in debt recovery across New Zealand, from early demands through to court proceedings and enforcement, and have put together a list of sensible steps to materially reduce risk and improve your ability to recover the debt if something goes wrong.

Put the arrangement in writing

Sounds obvious? However verbal agreements, short emails, or template documents not tailored to the actual loan taking place are a common source of disputes.

Clear documentation is one of the most effective safeguards in private lending.

A written agreement should clearly record:

- The amount lent and when it is advanced.

- Whether interest is payable.

- The repayment terms (i.e. frequency of repayment and the duration of the loan).

- Any security provided and how it may be enforced.

Clear documentation helps ensure everyone has the same understanding from the outset and strengthens enforceability of the loan if recovery action becomes necessary. Where loans involve significant sums, independent legal advice can help ensure the agreement is fair and not vulnerable to later challenge.

Define whether it’s a loan or a gift

A common issue in private lending is disagreement over whether money was a loan or a gift. This comes up constantly in family and relationship contexts.

If repayment is intended, it needs to be recorded at the time the money is advanced. After the relationship deteriorates is too late

Courts focus on the intention of the person making the advance at the time it was made. Written documentation, contemporaneous evidence, repayment behaviour, and the broader context of the relationship are all relevant. If repayment is intended, that should be expressly stated when the funds are advanced. Lack of clarity significantly increases the risk of dispute and difficulty of recovery.

Clear documentation and upfront discussion can avoid misunderstandings and reduce the likelihood of an expensive “loan versus gift” dispute later.

Set clear repayment terms

Uncertain or open-ended repayment terms are a common cause of dispute. Commitments such as repayment “when circumstances allow” are difficult to enforce and often lead to misunderstandings.

Loan agreements should specify how and when repayment is to occur. Clear repayment terms help manage expectations, reinforce that the advance is a loan, and place the lender in a stronger position if enforcement is required.

Consider taking security

Security can significantly reduce risk in private lending by giving the lender enforceable rights over specific assets if the borrower defaults. An unsecured loan relies entirely on the borrower’s ability and willingness to repay, which may change over time.

Depending on the circumstances, a loan may be secured over property or specific assets. Security does not mean enforcement is inevitable, rather, it provides leverage and encourages repayment. Any security should be properly documented to ensure it is effective and enforceable.

Think about recovery before the loan is made

Before advancing funds, it is important to consider how the loan could be recovered if repayment does not occur. Relevant factors include whether the borrower is likely to have assets available for recovery, whether the loan terms allow for prompt enforcement, and whether legal proceedings would be proportionate to the amount lent.

Considering recovery scenarios early helps inform decisions about documentation, security, and repayment terms and can improve your position if issues arise.

Act early if there are delays or missed repayments

Missed or delayed payments should not be ignored. While it may be tempting to allow extra time in private lending arrangements, particularly where there is a personal relationship, inaction can weaken recovery prospects.

Early steps may include seeking an explanation, reminding the borrower of their obligations, or issuing a formal demand if appropriate. Prompt action preserves leverage and may resolve issues before they escalate. If delays continue, early legal advice can help determine the most effective next steps.

Know your debt-recovery options

Private lenders in New Zealand have several debt-recovery options available if repayment is not forthcoming. Lower-value disputed claims may be pursued through the Disputes Tribunal, while larger or more complex claims may need to be brought in the District Court or High Court.

Where a loan is clearly documented and undisputed, summary judgment in the District Court or High Court may be available, allowing for faster resolution. If security has been taken, enforcement may also involve exercising rights against secured assets. Understanding these options early allows for a proportionate and cost-effective approach.

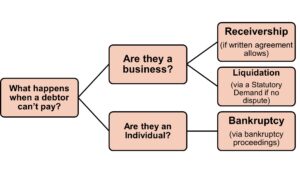

What are your options when a debtor still doesn’t pay?

Refer to the visual below for options.

How can we help?

Our experts regularly advise private lenders, businesses and individuals on structuring loans, enforcing repayment obligations, and taking early, pragmatic recovery steps when issues arise.

If you would like specific advice on your position, please get in touch.