Social media has become an incredibly effective marketing tool for all types of businesses. To appeal to social media users, businesses will often hire influencers to assist them in promoting their products or services. Influencers may assume that because they are simply a conduit for somebody else’s marketing, their liability may be limited. However, they could still be subject to legal claims from members of the public or regulators if their posts are considered false, misleading, or harmful. Similarly, the companies that engage the influencers can also be liable.

Image credit: E!, here.

A boom in the number and value of crypto-assets, especially the pop culture phenomenon of non-fungible tokens (NFTs), has given influencers and corporate brands alike a very real financial opportunity to leverage their follower and customer bases with high-value crypto-assets. However, the volatility of the crypto market and ubiquity of scams, means that the space is ripe for financial loss. A raging bull market, now followed by another freezing ‘crypto winter’, has led to some recent high-profile litigation over the failure of some crypto projects, such as EthereumMax (EMAX), which has placed influencers and the laws which regulate them in the spotlight. Notably, in that case, celebrity icon Kim Kardashian was charged and recently pleaded guilty to an action brought against her by US regulator, the Securities Exchange Commission (SEC).

This article considers what New Zealand law could apply if a claim, similar to that of EMAX, were brought in New Zealand against a local Web3 project and local influencers, and provides a breakdown of the law which could apply.

Background to the EMAX collapse

EMAX describes itself as an ERC-20 token on the Ethereum blockchain, a “community token” which “acts as the gateway to the EthereumMax Ecosystem” and “entry point into an all-encompassing decentralised ecosystem that rewards its users for holding and participation”. EMAX operated in a similar way to other crypto perk packages and traditional credit cards, promising access to cultural experiences, discounts, VIP ticket packages, rewards, and other lifestyle benefits. However, EMAX did not become self-sustaining, and prices began to fall in June 2021 as first movers fled the currency.

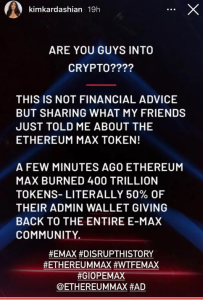

Image credit: Instagram/Kim Kardashian, here.

In January 2022 Kim Kardashian, Floyd Mayweather Jr, Paul Pierce, and others were sued as part of a larger claim against EMAX. The claim alleges that Kardashian and her co-defendants collaborated with EMAX to “misleadingly promote and sell” EMAX tokens via social media advertisements. Promotions by the company included an Instagram post to Kardashian’s 250 million followers (see below). In essence, the claim alleges that EMAX executives, with the assistance of celebrities, operated a pump and dump scheme.

Pump and dump schemes

Pump and dumps are a form of fraud, relating to financial investments, where the owner of a cheap stock uses certain tactics or actions (such as making false and misleading statements) to increase the price of their stock before selling the cheaply purchased stock at a higher price. Once the operators of the scheme ‘dump’ (sell) their overvalued shares, the price falls and investors lose their money as a result of acquiring these shares at an over inflated price.

The prevalence of cheap money, promotions by celebrities and businesspeople, get-rich-quick ideals, and social media have created ideal conditions for such schemes to thrive. Such is their prevalence in the crypto space, they have even got their own crypto-specific name – ‘rug pulls’. The dramatic crash into insolvency of the world’s second biggest crypto exchange, FTX, is another perfect example, with celebrities and sophisticated investors alike losing significant sums of money. Closer to home, the media speculated that festival ‘Juicy Fest’, which used NFTs as tickets, could be a scam. It should be noted that rug pulls do have their own crypto-specific characteristics (such as pre-mining), but for those looking to contextualise these schemes through the lens of traditional securities fraud, ‘pump and dump’ is a useful synonym. Over the last few years, and particularly since the beginning of the COVID-19 pandemic, millions of dollars have been raised in this way from the public, largely without compliance with financial markets law or disclosure requirements.

What is an EMAX token?

A crypto token is a digital asset, specifically a packet of data on a blockchain, verified by a network of computers. Tokens can be fungible (generic) or can be non-fungible (unique) – the latter known as an ‘NFT’. Tokens can be used to make purchases, exchanged for other digital assets, or invested. They come in a variety of forms: reward tokens, currency tokens, utility tokens, security tokens, and asset tokens. Some tokens provide incentives for the holder, such as access to specific digital content or governance rights.

EMAX described its crypto-asset as a “yield based token that rewards back its investors 2% of every transaction”. The EMAX Tokens are ERC20 tokens, a fungible token built on the Ethereum blockchain, but they are not otherwise associated with those who created the Ethereum protocol. EMAX allegedly launched with 2 quadrillion tokens, but due to the platform’s ‘tokenomics’ (the economics of the token), the number of EMAX tokens decreases irregularly when EMAX tokens are ‘burnt’. Tokens are burnt when they are transferred to an inaccessible digital wallet. By removing a number of tokens from circulation, the developer can manipulate supply and demand and increase the value. The burning of tokens works in a similar way to a share buy back by a traditional company.

The case against Kim

The causes of action against Kardashian and her co-defendants can be broadly categorized as engaging in:

- unfair, deceptive, untrue, or misleading advertising;

- unfair or deceptive acts resulting in the sale of goods; and

- aiding and abetting the commission of a tort.

These claims would be largely covered by the provisions of the Fair Trading Act (FTA) in New Zealand. The FTA is designed to protect consumer interests, prohibit unfair business conduct, and prevent three broad categories of undesirable market behaviour: misleading or deceptive conduct, unsubstantiated representations, and false representations.

Under the FTA, those advertising crypto-assets must ensure their advertisements are not misleading or deceptive, or likely to be misleading or deceptive. It is key that advertisements do not create a false impression about the goods or services which are being advertised. When advertising digital assets, advertisers must have reasonable grounds for making any claim. Unsubstantiated claims or representations about a product may give rise to a cause of action under the FTA.

The FTA defines representations broadly, covering any situation in which a person ‘in trade’ makes a claim about their product or service, directly or indirectly, verbally or in writing. Representations can even cover situations where those in trade omit key information about a particular product. Courts in New Zealand generally favour a broad interpretation of the FTA’s term ‘in trade’. While in differing contexts, New Zealand courts have confirmed that statements endorsing certain business activities may be ‘in trade’ if those statements are intending to promote the commercial interests of the parties involved. Given that Kardashian’s post is specifically noted as an ad, there is no question that she would be in trade according to our legislation. Similarly, her co-defendants sought to promote the commercial interests of EMAX for their own financial benefit. With that in mind, similar social media advertising is likely to be in trade and subject to the FTA.

According to the claim, Kardashian and her co-defendants promoted the “prospects of the company and the ability for investors to make significant returns due to the favourable tokenomics of the EMAX Tokens”. If Kardashian’s posts were false or misleading as to the tokenomics of the EMAX Tokens, such as in relation to the burning of tokens and the quantity of tokens, the FTA would likely be engaged.

Section 12A of the FTA prohibits making unsubstantiated representations in respect of, among other things: the supply or possible supply of goods; and the promotion by any means of the supply or use of goods. A representation is considered unsubstantiated if the statement-maker, when making the representation, does not have reasonable grounds for the representation, even if the representation is not actually false or misleading. If the statement-maker (in this case, the influencer) had reasonable grounds for making the statement, their liability would be limited. When assessing whether a statement-maker had reasonable grounds for their representation, the Court must have regard to all the circumstances, including:

- the essential nature of the goods;

- the content of the representation;

- any due diligence taken by the person before they made the representation;

- the extent to which the person making the representation complied with the requirements of any standards, codes or practices relating to the representation made; and

- the actual or potential effects of the representation on any person.

In the EMAX case, the actual effects of the social media posts are quantitatively discussed in the pleadings. The statement of claim shows that two days after one of Mayweather’s promotions of EMAX, the trading volume for EMAX Tokens spiked. Regardless of the evident impact of the posts, determining whether the representations made were unsubstantiated, false, or misleading will likely depend on the context of Kardashian’s briefing from EMAX and her own understanding of the product. It is currently unknown whether the defendants did any research into EMAX, or the tokens advertised within their posts. It is also unknown whether such posts would be compliant with any required standards, codes, or practices.

In any case, it is safe to say that if you are an influencer considering doing business with a crypto project, it would pay to do your due diligence and understand what you are promoting. Certainly, it would pay to require warranties and indemnities from the project as to the accuracy of information provided to you which you rely on when making statements to your followers.

Are cryptos ‘goods’?

Similarly, section 13 prohibits false or misleading representations in relation to the supply, or possible supply, of goods and services. The provision includes specific forms of representations, including relating to the kind and composition of goods. The obvious question in the case of crypto is whether a token is classified as a ‘good’.

Cryptos are not expressly mentioned in the FTA, nor are they discussed in legal commentary or case law concerning the FTA. However, the FTA broadly defines “goods” to include “personal property of every kind (whether tangible or intangible)”. In Ruscoe v Cryptopia the High Court established that cryptocurrency is personal property as it meets all four of the classic characteristics of property. Relevantly, the court in Cryptopia also highlighted that the purpose of cryptocurrency is to create an item of tradable value. In light of the ruling in Cryptopia, it is highly likely that crypto-assets could be considered as a good within the FTA framework.

Financial Markets Conduct Act

The Financial Markets Conduct Act (FMCA) may also be an option for New Zealand litigants facing a similar situation. The FMCA governs how ‘financial products’ are created, promoted and sold, and the ongoing responsibilities of those who offer, deal, and trade them. The NZ regulator that enforces the FMCA is the Financial Markets Authority (FMA).

Those undertaking or promoting crypto projects should consider whether their crypto will be captured by the FMCA or not, as the requirements of the FMCA are significantly more prescriptive than those of the FTA. If the crypto is caught under the FMCA, they may be exposed to much more serious penalties (such as imprisonment) as compared to the FTA. If a crypto is a financial product and the token is offered to retail investors in New Zealand, the offer is likely a ‘regulated offer’. If so, there are several requirements for the party issuing the token to meet under the FMCA including:

- Disclosure – The offeror must provide a product disclosure statement (PDS) unless the offer is wholesale. These are highly detailed and must contain certain prescribed information – this may not be practical for some projects.

- Governance – If the crypto is a debt security or managed investment product, the offeror will need to appoint an independent supervisor operating under a trust deed. This is likely to present real difficulties to decentralised autonomous organisations (DAOs), which by their nature have no centralised governance or management.

- Licensing – If the token is a debt security, managed investment product, or derivative, a licence for the issuer will be required from the FMA or the RBNZ.

- Financial reporting – This includes registering publicly available audited accounts,

From the perspective of those investing in crypto, the FMCA provides considerably more protection because the offeror of the crypto may be required to provide certain disclosures, be licensed by the FMA or registered as a financial service provider (FSP) registration, these provide more comfort than the more general FTA provisions.

Importantly for crypto projects and influencers, there are fair dealing requirements under the FMCA. Sections of the FMCA largely mirror many of the terms within the FTA provisions discussed above. The courts have adopted analysis of terms in the FTA when considering the mirrored terms of the FMCA. As such, cases considering misleading conduct, misrepresentation and in trade will be relevant. Similar to the FTA, claims made in the advertisements must also be able to be substantiated. The offeror must have reasonable grounds to believe, at the time of the advertisement, the information within the relevant advertisement is able to stand up to scrutiny. If an unsubstantiated representation is made during the course of advertising, that unsubstantiated representation will continue to be treated as unsubstantiated – even if it is discovered to be true or justified later.

Offerors must take care when comparing different financial products and only compare products that are similar enough to be meaningful. For example, term deposits should not be compared to managed investment schemes, because the two have significantly different levels of complexity, even though outwardly, they may both offer a fixed percentage return. Offerors should also ensure that promoting the benefits of a particular product does not overshadow potential risks. For instance, riskier investments in crypto cannot overpromote their comparatively higher returns. Offerors cannot overemphasise past performance as an indication or implication of future performance or returns and this should not be the main focus of advertisements.

When does the FMCA apply?

The FMCA only applies to ‘financial products and ‘financial services’. Each crypto is assessed on case-by-case basis to see whether it meets the requirements of a financial product or service. Often, cryptos have characteristics of a financial product without being an actual financial product. Concepts like yield-based tokens, crypto wallets, crypto credit cards and perks associated with token use have been derived from products available on traditional financial markets. Currently, the FMCA covers four categories of financial products being debt securities, equity securities, managed investment products and derivatives. However, the FMA (if necessary) has the power to make any other ‘securities’ subject to the FMCA (i.e. designate them as ‘financial products’). A ‘security’ is defined as “an arrangement or a facility that has, or is intended to have, the effect of a person making an investment or managing a financial risk”. This is deliberately drafted very broadly.

The FMA has confirmed that crypto-assets are debt securities, if investors holding a crypto-asset have a right to redeem that asset for money or be repaid money deposited to the platform. A crypto-asset is also an equity security if investors can buy, or have the option to buy, shares in an NZ company as a result of holding or acquiring that specific crypto-asset. A crypto-asset can be a derivative if the platform may be required to pay an amount in the future and the value paid out is derived from the value of something else. In these situations, investors may find protection within the FMCA.

The FMA has confirmed that ‘financial services’ can include crypto-asset exchanges, wallets, deposits, brokering and initial coin offerings (ICOs). If those financial services involve digital assets, the platforms will be subject to the obligations of the FMCA.

Interestingly, crypto-assets which give investors a right to redeem a token in exchange for certain crypto-assets, are not considered debt securities because the investor does not have the right to be repaid ‘money’. To use EMAX as an example, the developers and promoters behind the protocol may be providing financial services under the FMCA, but the EMAX tokens themselves might not have qualified as financial products as defined under section 7 of the FMCA.

Market manipulation

The FMCA also covers market manipulation. Subpart 3 was inserted to tackle situations where misleading information is disseminated to manipulate trading price and activity. As such, these provisions would likely be relevant in a case like EMAX. Importantly, sections 262 and 264 refer to a person rather than a person in trade. This widens the provisions to catch influencers manipulating the market who may not be caught by the FTA or other sections of the FMCA.

To be caught by the market manipulation sections of the FMCA, a person must have made a statement or disseminated information in which:

- a material aspect of the statement or information is false or materially misleading; and

- the person knew or ought to have known the statements were false or misleading; and

- the false or misleading information is likely to have one of the effects listed within s 262(c), such as: to induce a person to trade in quoted financial products or increase the price for trading in those financial products.

Criminal liability is imposed for the contravention of the market manipulation provisions, if the person knows that their statements are materially false or misleading.

The EMAX claim alleges that the celebrities were used to instil trust in uninformed investors to promote the financial benefits of a highly speculative and risky investment in EMAX Tokens. This was done in an effort to manipulate and artificially inflate the price and trading volume of the EMAX tokens. If the celebrity defendants made misrepresentations, they could be caught by the market manipulation provisions of the FMCA.

Situations in which an influencer boasts about the financial performance of a digital asset that is in fact doing well at that time, will likely result in difficulties for FMCA claims. The social media posts may encourage other investors and the price may be manipulated as a result. The influencer may then sell and encourage a dump. If the original statements are true however, establishing a breach of section 262 of the FMCA will be difficult.

Kim’s settlement with the SEC

Kardashian’s alleged breaches of US securities laws, failing to disclose all the information that was legally required for security endorsements (including the amount she was paid for the promotion) have cost her a US$1 million penalty. Additionally, she has agreed not to promote crypto securities for the next three years. While a significant sum for most, it is probably a drop in the bucket for Kardashian (who has a net worth of close to $2 billion).

In any instance, Kardashian’s case shows a willingness by regulators to enforce financial markets law against crypto influencers. Similarly, the Friel v Dapper Labs case shows that disgruntled private litigants might also claim damages for financial markets law violations. The Dapper Labs case involves a class action lawsuit in respect of the NFT project NBA Top Shot.

The weight of the investors’ own decision-making is likely to be an issue in pump and dump cases. Contributory negligence may offer some defence for crypto projects caught in such circumstances. When investors place their trust in non-financial advisors, especially in the context of a notoriously volatile market, some personal accountability will likely be important. The crypto market is inherently unpredictable, making many hesitant to invest in this asset class in the first place. The EMAX claim itself acknowledges the volatility of the market and labels the investors as uninformed. However, no responsibility is placed on the investor for their individual investment decisions. Whether this is fair or legally sound is yet to be tested.

Further, Kardashian’s post was clearly flagged as “not financial advice” and as an ‘#ad’. Whether such disclosure is sufficient in New Zealand will likely become more of an issue, especially for those posting information relating to specific financial products.

There is an emerging trend of financial educators using social media to provide investment tips about asset classes, investing and digital assets. However, on social media, the line between financial education and financial advice can be blurry. This is especially so when influencers/educators refer to specific investment strategies, markets, or investment apps. Informing followers with vastly different risk profiles, life stages and financial backgrounds about specific investments, may ultimately lead followers to make financial decisions. Ensuring that information is not taken as advice and subsequently relied on will be a difficult task for financial influencers. To avoid litigation, it is recommended for financial educators, influencers and those who are thinking of promoting digital assets to seek legal advice.

Conclusion

Relying on non-financial advisers, such as influencers, to make investment decisions is unlikely to be a profitable exercise for the majority. Those that benefit from pump and dump schemes are increasingly likely to find themselves caught by existing legislation, moulded to meet this emerging problem. For Kiwis affected by false or misleading representations in relation to crypto projects, even traditional businesses using NFTs, the FTA and FMCA are two potential avenues for redress, although currently untested. As discussed above, the legislation may not be entirely equipped to cover different crypto-assets and the actions of platforms utilising misleading practices.

Financial influencers, looking to educate rather than to encourage specific investment, may also find themselves caught by our consumer-focused legislation. Crypto project leads should also consider their liability in the eventuality their project does not come to fruition. As regulators race to catch up with the ever-evolving landscape of digital marketing and digital assets, managing the risks of the crypto market will be a key differentiator between those who succeed and those who lose out.